I’ve tried to help people understand the house buying process, but this is where the wheels usually come off.

For example, a younger friend of mine wanted to buy a home with her partner, and asked me for some help with the process. My advice was that their first step should be to check their credit files. It turned out that my friend knew this would be a problem – her credit was great, but her partner had had bad debts and defaults in years past.

I didn’t want to sound like the voice of doom, so I told her that the best thing to do would be to spend the next 6 months at least building his credit score back up; the problem was, they wanted to get their house as soon as possible.

They went ahead and filled in the online forms to find out how much they could borrow, and with their hopes raised, made their application. Of course, they were very disappointed when they were turned down.

Noddle decided I was two different people, and ‘single me’ had a better credit rating than ‘married me’. Woops!

It’s not hard to understand why – for them it felt like “close your eyes, cross your fingers and jump!” – but there’s not much chance in the equation. It’s a lot more rational than that.

You see, you may be a great gal/guy, but your bank doesn’t know that. On top of that, it doesn’t really care… it just wants to know whether you’ll pay it back. So it goes to someone else who’s been finding out all about you for years…

You may not think it fair – of course, my friend didn’t – that some shadowy commercial entities are gathering and storing information about us all behind the scenes. Put it that way, and it sounds more than a bit creepy, and yes, it can be unfair that credit referencing agencies (CRAs) can wield so much power over our lives, especially when they get things wrong. Still, think of it this way: would you lend money to someone you knew nothing about?

Why do they do it?

Credit scoring doesn’t have anything to do with how much you earn or whether you can afford your mortgage payments. It’s all about your record of paying back your debts.

When we started our house buying plan, I had a year and a half set aside for generating extra income, saving, and polishing up our credit ratings. Yes, we trashed our credit files formoney – opening bank accounts and credit cards for bank incentives and stoozing, but 6 months before we were ready to make an offer on a property, we stopped. Every credit card was paid off, and all of the searches on our files were left to expire.

By the time the bank did its credit scoring on us, we were absolutely spotless.

What can damage my credit rating?

It’s all about risk. Every time you apply for credit (inc. current accounts, loans, credit cards and mortgages), the lender searches your credit file, which leaves a ‘hard’ footprint that can be seen by others. Also, if you’re financially linked to someone else (via a joint bank account, mortgage or financial product) they will be searched as well, and vice versa. Starting to get the mental image of being frisked…

Lots of recent applications for credit makes you look like a risky proposition, as does a recent change of address. In fact, when we successfully bought our home and moved in, we found that our credit ratings had taken such a hit that we couldn’t pass the credit scoring for getting our pre-payment gas and electricity meters switched to a regular meter! Unfair? Well yes, but it’s all a bit ‘computer says no’ in this game, so we sucked it up and moved on.

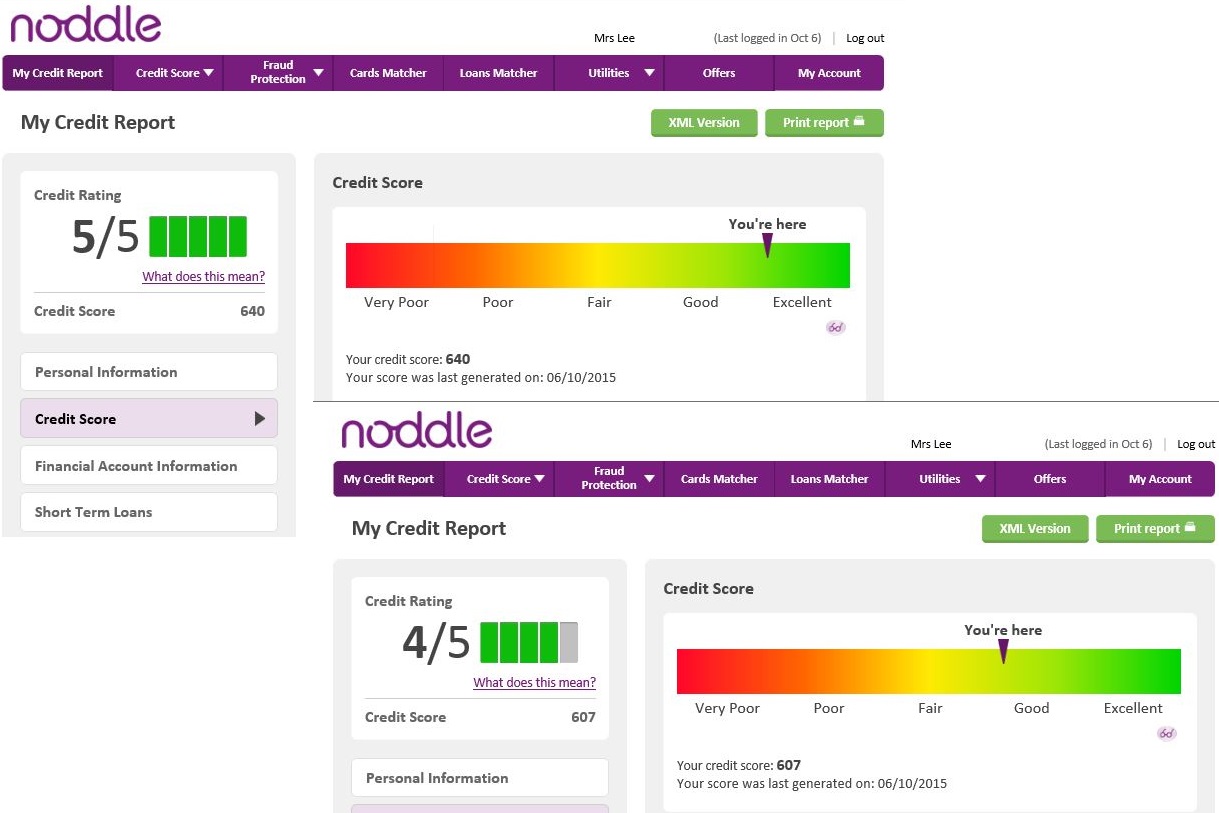

Want to buy a house? Check your credit files. In the UK there are four major CRAs – Experian, Equifax, Callcredit and Crediva. Don’t be fooled by ads for expensive subscriptions; you can get a copy of your credit report for £2. And don’t be scared into buying add-ons to boost the ‘score’ they’ve given you – there is no universal credit score. Each company assesses differently… but we still jump at the numbers they assign us as if they were our school exam results!

So what are you looking for in your credit file? Make sure there’s nothing wrong there – the CRAs can make mistakes, and you don’t want to be punished for their errors. Also, it’s useful to make sure there’s been no fraudulent use of your accounts or identity theft… and check that you’re not linked to anyone you’re not expecting. Ex-husband or ex-wife popping up there? Aaargh! Time to apply for a financial disassociation. By the way, you’re not linked to anyone or ‘blacklisted’ because of sharing an address – your financial association only comes from jointly held financial products.

Also, it’s good to know that you can ask your bank/financial institution to remove a search from your credit file if an error has been made on their part. I requested this recently after my bank’s website lost my current account application just after credit scoring me. No way was I taking the hit for two searches!

Can I improve my credit rating?

So, everything on your credit file looks familiar and ask yourself, would I lend money to a person with this record? If your credit record is less than perfect, then… change it!

Yes, it can improve, but you may need to dedicate a few months or more to making payments on time, correcting errors or just letting previous searches expire. Defaults expire after 6 years – searches by lenders take 6 months. Focus on clearing debts and making all payments on time, as well as avoiding new searches. Remember when I said above it’s all about risk? Well, older accounts appear less ‘risky’ to CRAs and lenders than brand new ones – if you want to shut some down, try to keep your oldest account open – you’ll look more stable.

Erm… does this sound like it’s too long-winded? Well, don’t look at it as an inconvenience; look at it as laying a foundation for your financial future. A mortgage is a long-term commitment, so why should anyone expect to rush into it? If you want it all right now, you should have laid the ground work in the past… if you haven’t, then start laying it for the future.

Over to you…

Let me know what you think – have you had good or bad experiences with the credit referencing agencies?

By the way, this is the third part of my mortgage series – read part 1 and part 2.